[ad_1]

A view on the ENAMI’s (Nationwide Mining Firm) copper cathodes plant at Tierra Amarilla city, close to Copiapo metropolis, north of Santiago, Chile, December 15, 2015. REUTERS/Ivan Alvarado/File Photograph

LONDON, Oct 21 (Reuters) – This was the week Physician Copper turned disorderly.

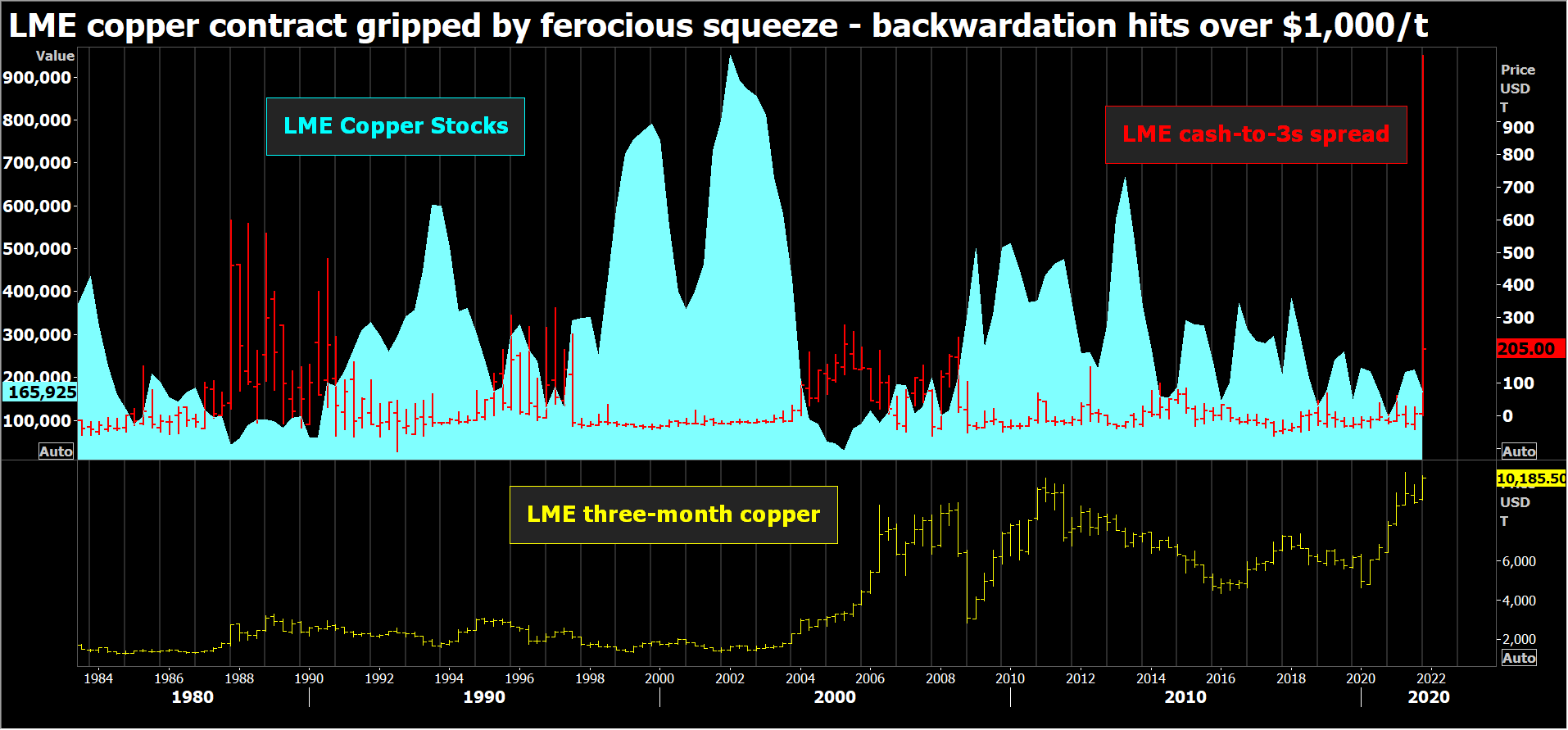

The London Metallic Change (LME) was compelled to use the restraints as a ferocious squeeze rocked the market, with the premium for money metallic spiralling uncontrolled to an unprecedented $1,103.50 per tonne at one stage on Monday because the change’s month-to-month immediate date descended into chaos.

The London copper contract has been sucked right into a shares vacuum after the quantity of obtainable metallic within the LME’s international warehouse system sank to only 14,150 tonnes final Friday, the bottom since 1974. The remainder of the 181,400 tonnes had been cancelled in preparation for load-out, that means it was off the desk when it comes to the month-to-month reconciliation of bodily positions.

Who’s grabbed all of the copper?

Trafigura for one. The buying and selling powerhouse mentioned it had certainly been hoovering up LME shares however mentioned that others had additionally been concerned within the string of inventory cancellations that depleted accessible tonnage from greater than 168,000 tonnes in the course of September.

The squeeze has, inevitably, evoked unhealthy reminiscences for the copper market, particularly the Sumitomo scandal of the Nineties, a protracted interval of manipulation centred on rogue dealer Yasuo Hamanaka.

The comparability is comprehensible however the present market dynamics usually are not these of the final decade of the 20 th century.

TROUBLE WITH TOM

What hasn’t modified between then and now could be the LME’s tolerance for giant dominant positions, each paper and bodily within the type of registered shares.

That is traditionally hard-wired into the 144-year-old market’s DNA as a result of it has at all times been the place the world’s largest industrial metals gamers have performed their enterprise.

Nevertheless, the LME’s light-touch regulation conforms to the British monetary mannequin.

The present LME rule-book, permitting dominant positions however with restrictions on how they’re traded, was written by Alan Whiting, government director of the UK Treasury’s regulation and compliance division earlier than he was parachuted into the LME in 1997 to kind out the post-Sumitomo mess.

The draw back of this method is that the LME solely intervenes when the market is on the purpose of breakdown, or in regulatory communicate, turns into disorderly.

The chaos meter, because it have been, has at all times been and stays the LME curiosity that’s “tom-next” , which is the price of rolling a brief money place in a single day. It went supernova on Friday, buying and selling out to $175 per tonne backwardation and hit triple figures once more on Monday and Tuesday.

At which stage the LME introduced it could cap the unfold at 0.5% of the day prior to this’s money value – round $50 per tonne – – or at 0.25% within the case of huge positions amounting to greater than 80% of obtainable shares.

Since accessible shares, at present negligible, are the standards for figuring out dominant lengthy money positions, it is no shock that as of Monday’s shut there have been 5 of them, two of them lengthy to in extra of 90% of obtainable LME shares.

SPECIAL MEASURES

The LME, which mentioned it had been “monitoring the continuing tightness within the copper market with Change inventories falling and close by carries tightening”, evidently determined the chaos was solely going to proceed as shorts tried to roll their means out of hazard.

Or quite its Particular Committee did.

This physique with the uninspired title was created to keep away from the potential for conflicts of curiosity that had dogged the total LME board when it used to determine on market interventions within the pre-Sumitomo days.

Chaired by Phillip Crowson, beforehand a long-standing LME director, the “specials” embrace LME chairwoman Homosexual Huey Evans, who additionally sits on the UK Treasury board, LME Clear board member Marco Strimer, arbitration lawyer Barbara Dohmann QC and unbiased LME director Dr Herta Von Stiegel.

Gavin Prentice, at present chairman of the LME’s Consumer Committee, joined the Particular Committee final month, presumably to spice up practitioner information.

Whereas that is a number of regulatory and authorized firepower, it nonetheless operates throughout the LME’s and London’s laissez-faire market ethos.

TROUBLE WITH COPPER

It is clear from each LME and Trafigura statements that the 2 have been in regulatory dialogue concerning the dealer’s copper positions and its draw on change shares.

Trafigura seems to glad LME compliance officers that it has a official motive for purchasing a lot copper from what is meant to be the market of final resort.

Cynics will scoff on the firm’s quoted declare the metallic is required to fulfill buyer wants in China and Asia, however international change shares of copper have been simply 312,200 tonnes on the finish of September with Shanghai shares sitting at a multi-year low of 43,500 tonnes.

Examine and distinction with the early Nineties copper market, when the LME warehouse system – rather more geographically concentrated than it’s now – held greater than 600,000 tonnes at one stage. Certainly, the ballooning prices of supporting the copper value in a surplus market have been what did for Sumitomo’s Hamanaka in the long run.

If that form of surplus is obtainable in the present day, why has it not proven up?

Backwardation is meant to draw metallic however this week’s deliveries into LME warehouses have to this point amounted to a meagre 9,775 tonnes regardless of the most important incentive available in the market’s historical past.

The unwelcome chance is that the world has run out of freely accessible copper. Or, if there’s metallic on the market, it’s stranded by document excessive freight charges, one other COVID-19 variant on copper crises previous.

DYSFUNCTIONAL SUPPLY CHAINS

Which may sound surprising however the tin market is already there, registering its personal outrageous $6,500-per tonne cash-to-three-months backwardation in February on account of a depleted provide chain.

European zinc smelter cutbacks are sending ripples of tightness from the bodily to the LME market, the place three-month metallic final week hit an all-time excessive and spreads are additionally backwardated.

LME lead should not be in backwardation however it’s. There’s tons and plenty of lead sitting in Shanghai however super-high container charges are maintaining it trapped in China.

Industrial metallic provide chains are at present dysfunctional in a means that hasn’t been seen previously as a result of it is the results of an unprecedented pandemic.

The world is a really totally different place from what it was simply a few years in the past not to mention the Nineties.

Is the present dearth of LME copper a manufactured scarcity or one other signal of a broader supply-chain disaster?

We will discover out very shortly since each accessible tonne of copper needs to be heading in direction of an LME warehouse to capitalise on the document supply incentive.

For now tom-next has stopped flashing pink, slipping again into extra orderly contango Thursday morning, suggesting the turmoil has abated.

But when change shares do not rebuild, the LME Particular Committee goes to have its work lower out.

The opinions expressed listed below are these of the writer, a columnist for Reuters.

Enhancing by Kirsten Donovan

Our Requirements: The Thomson Reuters Trust Principles.

[ad_2]

Source link